Spending when uncertainty is high

I recently stumbled across David Rogers’ book The Digital Transformation Roadmap and found myself nodding in agreement with page after page. Many of the points and arguments Rogers advances are expressed in my own Continuous Digital, I see two differences. First off Rogers is an established academic at Columbia Business School, so he approaches the topic with rigour. Second, he tackles the subject from a digital business starting point, Continuous Digital grew out of the agile and #NoProjects movements. Still, they end in the same place.

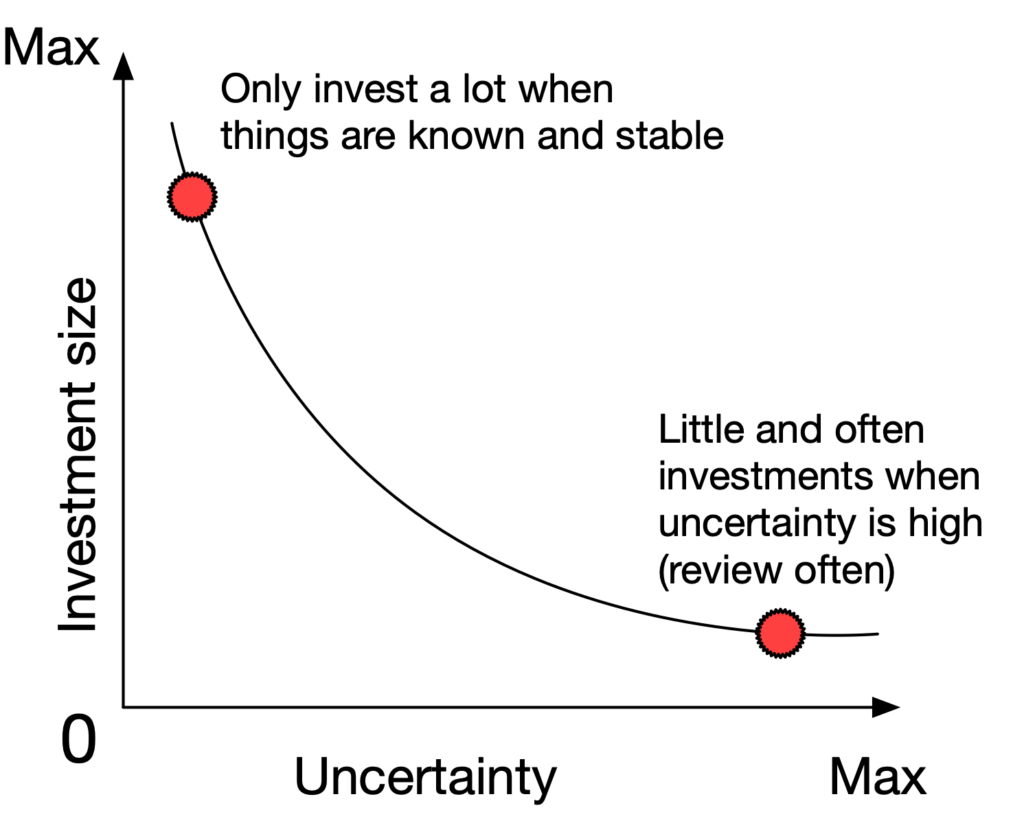

One of his models keeps coming up in my discussions with Product Leaders again and again, he calls it the Rogers Curve. Like I do in Continuous Digital he points out that the venture capital industry funds technology products very differently to corporations. A corporation minimises risk by doing lots of up front research, validation and planning. Then, if everything checks out authorises big expensive projects. When things go wrong (because the research missed something, validation was flawed, plans were too optimistic, delivery was more difficult than expected, or, importantly, the time spent making sure the money wasn’t misspent delays the work so much it has lost value) then it is difficult to cancel work because the momentum is high.

Conversely, venture capital firms invest far smaller sums of money on far less evidence, research and planning. Additional funding is only given if ventures make progress on validating the model and delivering. VC firms offset risk by placing many “small bets” which they expect to lose. As long as a few bets succeed big they will make money overall even if they lose most of the time.

In Continuous Digital I argue that all technology work should adopt this model. Rogers suggests something slightly different. His Rogers Curve combines the two. He says: when uncertainty is low then use the traditional project model with the upfront validation. However, when uncertainty is high then use the VC model.

Uncertainty might come from using a new technology, entering a new market, creating a new product for an existing market, or some other source. Naturally, certainty comes when none of these is true. Which begs the question: “why bother?”

Remember that much uncertainty is actually risk. According to economists: profit is the return for risk. If you eliminate the risk then eliminate the profit.

Imagine for a moment you see a market opportunity. You see that existing technologies can be repurposed to meet this opportunity. You easily ascertain that potential customers want the product and will pay. Best of all, you see that little work is needed to seize this opportunity. The stars align. You are in business. But, if you can see this opportunity and how to fill it the chances are others can too. If they haven’t already done this then they can quickly copy you. You have no defence from competitors. No risk, no reward.

Back to the Rogers Curve. This provides a great way of looking at future work: do we feel safe? Yes, then big up-front investment. Or do we feel uncertain, exposed to risk? In which case give it a little funding, review and refund often. And be ready to walk away.

One problem I do see with the curve is the “But we know” problem. Specifically, I remember one executive sitting opposite me and saying “We know what needs doing. We know who are customers are and what they want.” Needless to say they didn’t. The company became a lot more successful when they started acting as if they didn’t know (and sacked that executive.)

This happens all the time. People and companies are sure they know what is wanted – cognitive biases are at work. Version 2 technology rewrite projects are a classic example. These always have big problems. There is an assumption that the “only thing” version 2 needs to do is everything version 1 does, just on new technology. These projects always end up in trouble (but that is another post.)

Part of me thinks this curve is unnecessary because the little-and-often funding model will work in a certain world just as it works in the uncertain. But, corporations aren’t set up to work like that. Corporations are set up to fund and run big projects with lots of upfront work. In other words: corporations are not optimised at doing lots of small.

Jumping to a new model in one go is hard. Far better for the corporation to carve out some innovation money and a ring fenced a unit to spend the money. Call it an innovation unit, a lab, an incubator or whatever. Within this unit manage investments differently using a VC-style governance process. The money needed will be far less than one big traditional project to start with.

This unit can accept small innovative ideas with little market research, validation or planning. The minimally viable teams which are funded here are tasked not just to build the thing but to validate the ideas, exploring options, understand potential customers and everything else a start-up would do.

Now at this point some readers will be saying “We do that.” As Rogers points out, and I’ve seen myself, companies do do this but only sometimes. They don’t do it systematically. Nor do they do it repeatedly. Running these types of initiative, and more importantly governing them, is itself a skill set and process which needs developing itself.

Many companies can point to instances of innovative products managed in an innovative way. But such initiatives have to fight through a system which is designed to stop them. They succeed despite the system not because of the system. How much more successful could the company be if it created support mechanisms?

Spending when uncertainty is high Read More »